Unlocking the VA Home Loan Advantage for Veterans

Many veterans believe homeownership is further away than it really is. In reality, the path may be more accessible than expected with the benefits available to those who’ve served.

One of the most overlooked advantages of this loan program is how much it can reduce upfront and ongoing costs. Here are a few key ways it can make buying a home easier:

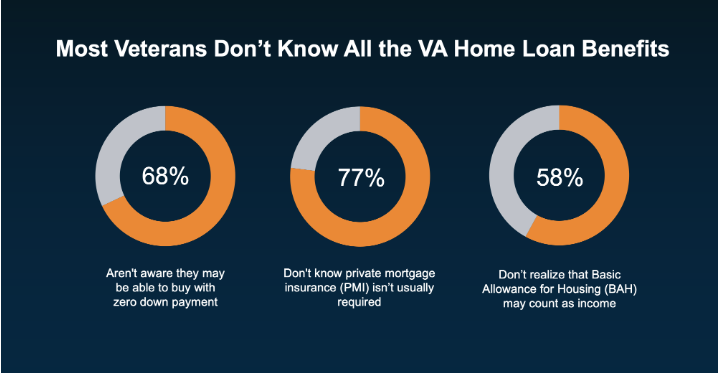

1. Little to No Down Payment

One of the biggest misconceptions is the need for a large upfront payment. Many buyers assume they need $10,000–$20,000 saved, when in many cases, financing is possible with little to no money down.

2. Reduced Closing Costs

There are limits on certain fees, which can help lower what you’re responsible for at closing. That means less out-of-pocket expense and less time needed to save before purchasing.

3. No Monthly Mortgage Insurance

Unlike many conventional loans, this program typically does not require private mortgage insurance, even with a minimal down payment. That can translate into meaningful monthly savings over time.

4. Income Strength from Military Benefits

For active-duty service members and qualifying reservists, housing and subsistence allowances may be considered as part of income. Since these benefits are non-taxable, they can strengthen qualifications and increase purchasing power.

The Takeaway

This benefit was created to support long-term homeownership and financial stability for those who’ve served. With the right guidance, it can open doors sooner than many expect.

If you or someone you know has served and is exploring homeownership, the Price Group is here to help you understand your options and move forward with confidence.