Adjustable-Rate Mortgages: A Smart Choice—or Not? Here’s What to Consider

If you’ve been house hunting lately, you know affordability is still a big challenge. That’s why more buyers are exploring adjustable-rate mortgages, or ARMs. They can be a smart way to lower your monthly payment upfront - but they come with some trade-offs you should know about.

What Is an Adjustable-Rate Mortgage?

Let’s start simple. A fixed-rate mortgage keeps your interest rate - and monthly payment - the same for the life of the loan. An ARM starts the same way, with a fixed rate for a few years, but after that, your rate can go up or down depending on the market.

Think of it like a rollercoaster: the beginning is smooth and predictable, but after a few years, there could be some bumps.

Why ARMs Are Gaining Attention

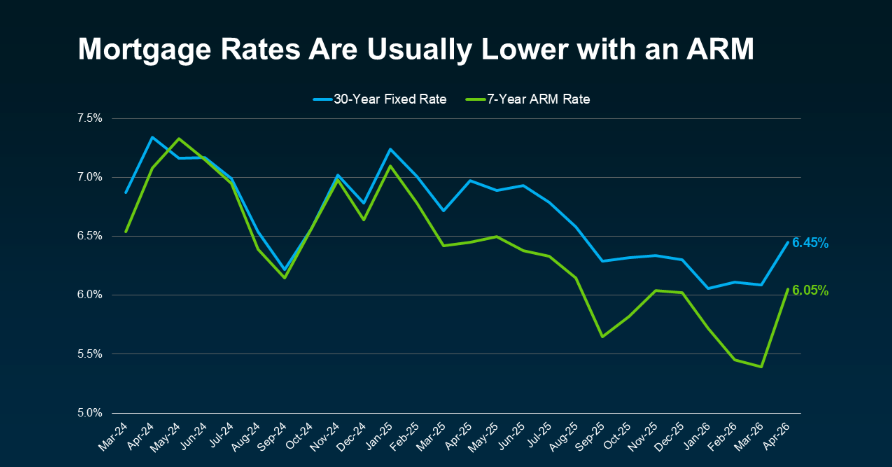

The main reason buyers choose ARMs? Upfront savings. Initial ARM rates are often lower than 30-year fixed rates, which means a smaller monthly payment - or the ability to afford a slightly bigger home.

For some buyers, that could mean saving around $150 a month. That’s real money you can put toward your home, or just use to breathe a little easier financially.

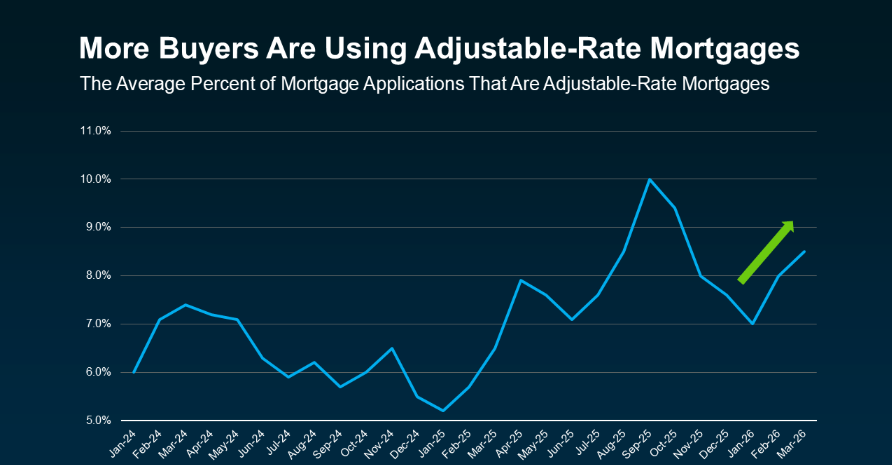

More Buyers Are Considering ARMs

These loans are growing in popularity. That doesn’t mean they’re perfect for everyone - but they are helping some buyers get into homes they otherwise might not be able to afford.

If the history of ARMs makes you nervous, take a breath. Today’s lending standards are much stricter than they were during the housing crash. Lenders now make sure borrowers can handle payment increases, so ARMs today aren’t the risky loan they once were.

The Trade-Offs

Here’s the reality: ARMs can make your home more affordable right now, but your monthly payment could rise later. They often make the most sense if you plan to move before the rate adjusts—or if you expect your income to grow over time.

And remember: there’s no guarantee rates will go down in the future, so refinancing isn’t always an option. That’s why it’s smart to think through your plan, your long-term earning potential, and work closely with a trusted lender.

The Takeaway

ARMs can be a helpful tool for today’s buyers, but they’re not a one-size-fits-all solution. The key is understanding how they work, the risks involved, and whether they fit your personal plan.

Talk to a lender you trust before making a decision - so you know you’re making the move that’s right for you and your family.